Back in February the Department of Justice filed a civil suit against Standard & Poor’s ( MHP –Analyst Report ) alleging that S&Pengaged in a scheme to defraud investors in structured financial products known as Residential Mortgage-Backed Securities (RMBS) and Collateralized Debt Obligations (CDOs).

The news sent shockwaves through the sector and gave MCO a 30% haircut from its high. To be clear, Moody’s is a competitor of S&P and one of the three major CRAs in the world. There may have been good reason to react that way, but it was no doubt overdone.

Shares have recovered about 80% of that selloff, but there might be even more upside from these levels.

A Necessary Niche

Moody’s is an essential component of the global capital markets. Their credit ratings, research, tools and analysis are a trusted source for millions and help determine risk allocations for everyone from average investors to sovereign nations.

The average credit rating of a company (or countries) debt directly affects what interest rate they have to pay to borrow money and help those lenders understand just how much risk they are taking on. Ratings are required by many investors to even entertain any cash outlay.

Moody’s one of three major agencies that offer this service and they have done so for over a century. This is a company that reported revenue of $2.7 billion in 2012 and employs approximately 6,800 people worldwide in 28 countries; they’re not small potatoes.

The world is not only becoming more integrated, but a great deal of our lives and the stuff we buy (houses, etc) are becoming securitized and need the services of Moody’s to give the public a sense of value and risk. Securitization of rental properties are an up and coming industry that will require Moody’s services. Blackstone and Deutsche Bank are introducing the first REO to rental securities and someone has to “rate” their risk.

The reality is that business is forced in a sense to use Moody’s services and the greatest irony here is that when S&P downgraded U.S. debt (which is what they should have done) they got slapped with a lawsuit (most likely unrelated, but still odd in my opinion).

The bottom line is that Moody’s in a completely different entity when compared to S&P or Fitch. Moody’s makes their decisions based on their own models and assumptions. The models are obviously not fool-proof, but unless Moody’s participated in a grand scheme to defraud millions of investors (which I don’t think they did) or was in cahoots with S&P, I don’t think they are going anywhere; in fact, I think they will continue to flourish!

If the marketplace believed that Sotheby’s was artificially inflating prices, then they either don’t pay the price or shun Sotheby’s altogether.

In the subjective, intangible world of high finance, there are NO absolutes.

Strong Earnings and Revenue Growth

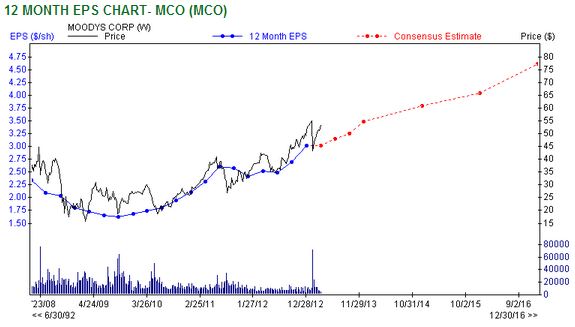

Moody’s reported upbeat fourth quarter results in early February, showing strength in new domestic debt issuance and improving clarity over regulatory climate in Europe.

They earned 75 cents per share, a 62.8% jump from the year-ago quarter and beat the Zacks Consensus Estimate of 70 cents by 7.14%. The report marked the fourth consecutive quarter of positive earnings surprises with an average beat of 10.4%.

The better-than-expected earnings were primarily driven by 33.0% surge in revenues and 53.7% jump in operating income.

Based on the strong results, Moody’s provided optimistic guidance for fiscal 2013. Moody’s expects 2013 revenues to grow in the high single-digit percent range. Operating margin is projected to be between 46% and 47%. Earnings for 2013 are expected to be in the range of $3.45 to $3.55 per share.

The Zacks Consensus Estimate for fiscal 2013 increased 9.1% to $3.49 per share as most of the estimates were revised higher over the last 60 days. The current estimate is within the guidance range provided by Moody’s. For fiscal 2014, the Zacks Consensus Estimate has again increased to $3.81 per share.

The long-term expected earnings growth rate for Moody’s is 14.0%, which easily justifies their forward multiple of 15 in my opinion.

The Charts

Moody’s has been in a bullish ascending channel sings the correction in early February. Shares never closed below the 200 day moving average and the 50 day moving average still remains firmly above the 200, both positive signs for the stock.

The current 50 day simple moving average of $50.54 coincides with past support in the current short term trend. Looking below that, traders can also use the 50 day WVAP of $48.53 as strong support. The VWAP is so much lower than the regular 50 day average due to all the volume that changed hands during the S&P debacle.

To the upside, look for a target of $55.14, which is just under the 52 week high of $55.58. That might be an area to take small profits. If shares break through that level with better than average volume, we could see a breakout run of 5% or so.

Moving Forward

Earnings are due out April 25th and with its Zacks Rank of 1 and positive ESP of $4.65%, there is a strong likelihood that they will beat the Zacks Consensus. The company has already offered positive guidance for the year, we need to see that stay intact and for revenues to be growing as well.

Moody’s is certainly a stock I wouldn’t mind owning here.

Jared A Levy is one of the most highly sought after traders in the world and a former member of three major stock exchanges. That is why you will frequently see him appear on Fox Business, CNBC and Bloomberg providing his timely insights to other investors. He has written and published two tomes, “Your Options Handbook” and “The Bloomberg Visual Guide to Options”. You can discover more of his insights and recommendations through his two portfolio recommendation services:

Zacks Whisper Trader– Learn to buy stocks likely to have robust earnings BEFORE they report.

Zacks TAZR Trader – Technical Analysis + Zacks Rank. Best of both worlds approach to find timely trades.

Follow Jared A Levyon twitter at @jaredalevy

Like Jared A Levy on Facebook